Investors have PULL too

On the subtleties of Projects

The PULL framework defines who would be weird not to buy from us.

It defines a person who is trying to do something - we’ll call that thing a Project - and this person is in a situation where they can’t do nothing, can’t delay the Project, can’t do something other than the Project, and can’t do the Project with another solution. In other words, this person is stuck - when we show up, they rip the product out of our hands.

Many other people, of course, could buy from us. We would solve their problems and provide them value. But these people could also do nothing, or buy something else. Given all the other things they could do or buy, it would be weird if they bought from us. We have to convince them, and they can just not buy. Which is why every fast-growing startup finds PULL.

These Projects, though, can be tricky. Think of them like “jobs to be done” or “intentions.” Projects define the shape or substance of what a person is trying to do / accomplish in any given moment. They are often quite nuanced.

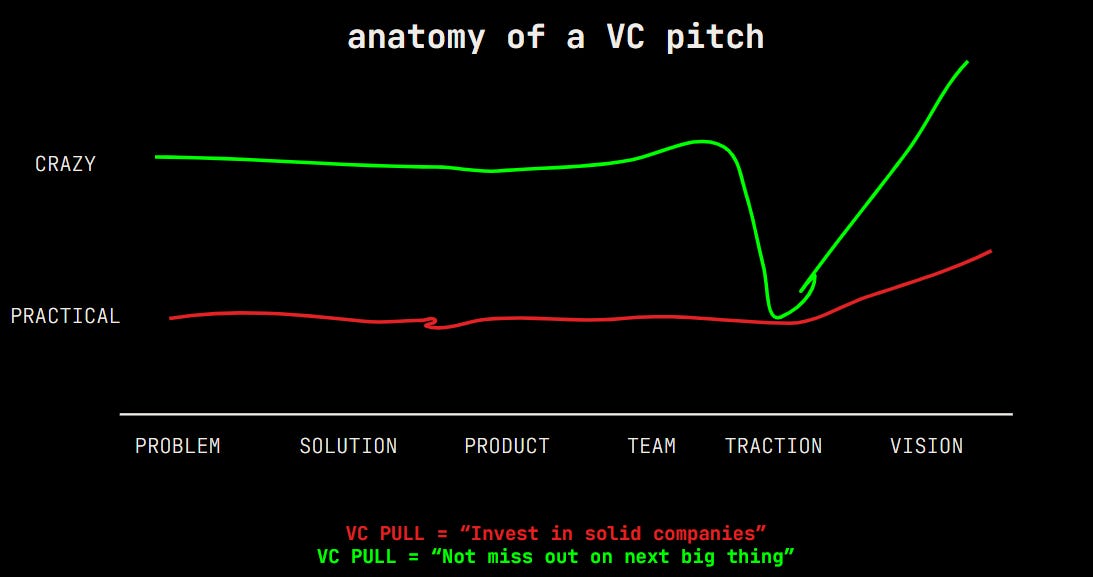

One way I explain how nuanced Projects can be is by talking about (gasp) your investor pitch. When you pitch a VC, your pitch expresses your theory of a VC’s Project.

If you read this newsletter, you’re probably the kind of founder who aspires to build a solid, fast-growing business with strong fundamentals and massive upside opportunity. Your pitch conveys this with defensible logic and rigor - and underneath that is the implicit belief that investors’ Project is “invest in solid teams with strong traction and a promising path forward.”

It turns out, this is almost certainly not VCs’ Project. Instead, their Project is closer to “not miss out on the next big thing.”

Which leads to a totally different pitch (not to mention fundraising process):

“Invest in a solid team with strong traction” → The “main character” of your pitch is going to be your current state: the problem you’re solving, your current traction, etc. And you’re going to share the “big vision” as a supporting character.

“Not miss out on the next big thing” → Your pitch is going to revolve around some nearly-insane massive story about the future, and you’re going to use your current state as a small piece of supporting evidence for that story.

I’ve drawn this diagram out multiple times to explain the two kinds of pitches:

The practical pitch makes sense… and generates yawns. And you tend to misdiagnose these yawns as reason to ADD MORE LOGIC AND DETAIL! Nope - you have to reinterpret what investors want, so you can wind up with a pitch that works, so you can get back to actually building the business.

See how nuanced Projects are? Even when we can all see VCs investing in startups - that’s really their core job, it is an observable thing we can all watch them doing - we tend to misinterpret their true Project. And when we subtly misinterpret their Project, it leads to a TOTALLY different pitch (and outcome).

The same, of course, is true of customer Projects. For example, both Gusto and Rippling watch companies struggling to pay their employees using their clunky payroll systems, but frame the “projects” in the buyers’ minds totally differently: One says “make HR delightful,” the other says “automate all HR + IT tasks”. This leads to different product architectures, ICPs, growth rates, and everything else.

What exactly are your customers trying to do?

One of my favorite parts of Friday is getting a newsletter from Rob! Awesome stuff! PULL can be applied to almost any situation

Is this just a speculative example or is it based on deep understanding of dozens of real investors (any biases towards stage or geography)?